ENERGIZED: Investment Insights on Energy Transformation

Edition 19

Flash Analysis: Energy Implications of the Iran War, Days 1-4

3 March 2026

Please note: This newsletter is for general informational purposes only and should not be construed as financial, legal or tax advice nor as an invitation or inducement to engage in any specific investment activity, nor to address the specific personal requirements of any readers.

Key Takeaways:

As Iran declared Hormuz closed, European gas benchmarks doubled over just 2 days, reflecting Qatar’s central importance to global LNG markets

The oil market reaction to this supposedly doomsday scenario has been notably more muted, reflecting China’s stockpiling and weak underlying fundamentals

We expect the bombing campaign to be short and sharp (~1-2 weeks) with oil and gas prices remaining elevated and volatile

A swift victory declaration will then pull benchmarks back down sharply to new trading ranges above pre-war levels: €35-40/MWh (TTF gas), 90-100 p/th (NBP gas) and $70-75/bbl (Brent oil)

Gas prices will likely retain a post-conflict Hormuz risk premium, pulling up power and food prices, impacting inflation and potentially interest rate trajectories

European energy security was already under urgent scrutiny; this will further motivate the buildout of local generation and storage capacity, and support greater focus on electrification of heat and transport

Hence this conflict further strengthens the strategic rationale for investing in clean energy infrastructure manufacturers, producers and flexibility providers

War objectives and timeline

As we write, we are now on Day 4 of the US-Israeli war on Iran. This war was expected, but the impact has still been significant and the situation remains very dynamic. Based on statements by Trump, Netanyahu, Hegseth and Rubio, the key objectives are:

Eliminate Iran’s perceived existential threat to Israel (there is no credible threat to the US)

Decapitate the regime from top down to paralyse effective decision making in Iran

Eliminate Iran’s military capabilities to ensure that whoever takes over is toothless and remove the ability for a quick military rebuild and/or rearmament of proxies

Further reduce any remaining nuclear developments following the major campaign on nuclear sites in June 2025

Trump will be very keen for this to be a short, sharp conflict for which he can quickly declare victory. Hence regime change is not a stated military objective, but dared on the Iranian people instead. That process cannot be controlled via aerial attack alone - and this is clearly not going to be a boots-on-the-ground conflict.

Iran is not Hizbullah or Hamas; it is a major regional power that has been building up its capabilities for decades. So despite the overwhelming force, fulfilling all objectives could still take some weeks. But a short deadline for the bombardment enables Trump to call himself the hero, draw a line and move on. That’s why the Americans are going all guns blazing to achieve these key objectives ideally in a week or no more than two. Especially now that Iran has played the Hormuz card hard and early, increasing the risk of unintended consequences.

In objective, design and execution style, this is as much an Israeli war as an American one. The Israelis have longed wished and planned for this golden opportunity to finally take the ultimate prize: inflict as much damage as possible on the Iranian regime and its associated institutions, the Revolutionary Guards and the Quds Force. They prefer short, sharp wars too, but equally they will not want to miss the chance to totally destroy Iran’s military and nuclear capabilities. So they may push Trump to allow a slightly longer bombardment. We are witnessing the textbook Israeli tactics previously practiced on Iran’s proxy allies: eliminate senior political and military personnel to decapitate the leadership and paralyse decision making, while in parallel rapidly eliminating military capabilities to make any successor toothless and compliant. We have seen the latter in Syria over the past year and something similar in Venezuela where the regime was left effectively intact but subservient to US power.

While they cannot ultimately control who takes power in Iran, the goal will be to ensure that it will be largely immaterial because whoever it is will have no cards left to play in the regional power struggle. Israel has already vastly reduced Hizbullah’s capabilities and now that the gloves are off with Iran, it is going in to finish that job. Regime change in Syria in late 2024 also removed another key Iranian regional ally. All these preceding events led inevitably to this existential moment for the Iranian regime.

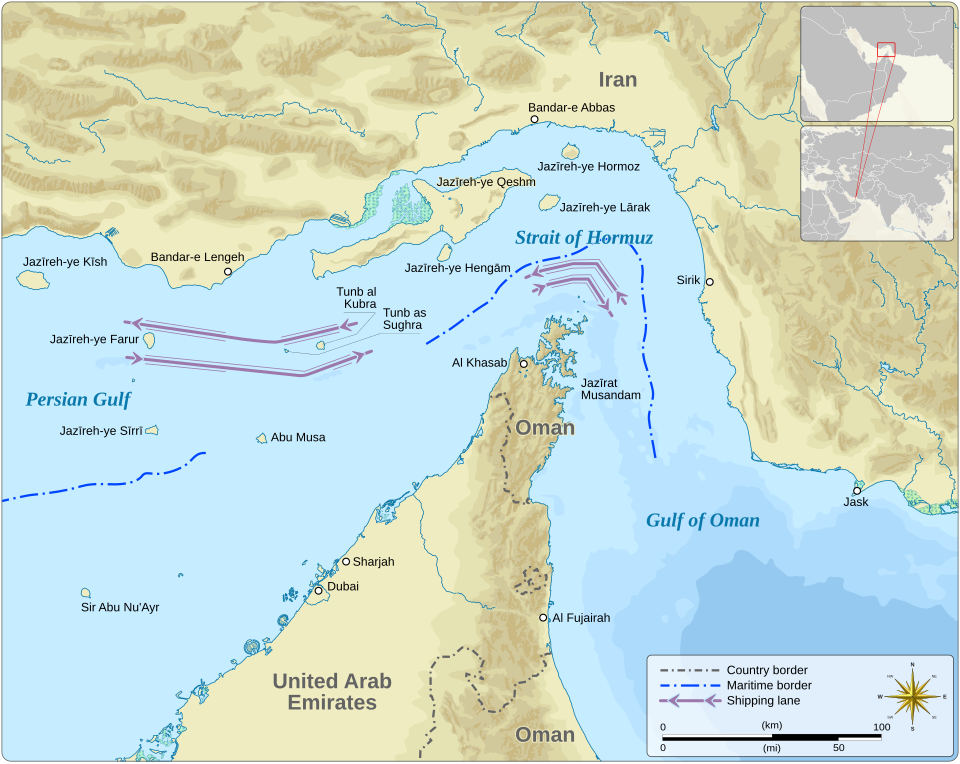

The world’s oil and gas chokepoint

Iran has chosen to play the Hormuz card early - hardly surprising given the rapid decimation of its leadership over the past 4 days.

The risk of the Strait of Hormuz being closed has been debated by analysts for decades. Closure is a lose-lose scenario for all exporters, including Iran, so it always seemed implausible. That is, until the regime - or what is left of it - has nothing more to lose.

That debate has always focused on the risks to the oil market. Yet so far, Brent has only peaked at around $85/bbl - much higher than a week ago but hardly the stratospheric levels feared for this scenario. The real action has been in gas benchmarks, which in Europe doubled in less than 48 hours, first moving on the outbreak of war and then on Qatar’s enforced pause in liquefied natural gas (LNG) production. It is hard to understate Qatar’s importance to the smooth functioning of global LNG and therefore gas markets. It is arguably much more than Saudi Arabia’s importance to oil markets.

Strait of Hormuz. Source: Wikimedia Commons

The Qatari pause removes a huge chunk of global gas supply - up to one fifth of the LNG market. Somewhat ironically, beneficiaries of the gas price spike may include US LNG exporters - although contracts are typically on long-term fixed prices. While oil can be strategically stockpiled for long periods (as China has been doing in preparation for this scenario), gas storage is more seasonal. The timing at the end of the winter means that European gas inventories are around their lowest point of the year, exacerbating the sense of risk. Normally these inventories would be rebuilt over April-September. Absent geopolitics, the market was looking increasingly well supplied. But now that restocking will likely be considerably more expensive.

For energy markets, the critical question now is how long Hormuz will remain impassable. That in turn depends on how quickly the US and Israel eliminate Iran’s military, missile and drone capabilities. The US will be particularly keen to see maritime traffic resume as quickly as possible, to avoid a prolonged disruption to energy markets. Trump may not be known for consistency, but he has always wanted to keep oil prices down, to minimise inflation and interest rates. He is already overtly trying to talk oil prices back down.

Yet another fire is lit under European energy security

The most secure energy is:

The energy you never even use (efficiency)

Produced domestically, as close to demand as possible

Harnessed from local resources rather than relying on continuous fuel imports

Produced by decentralised, diffuse infrastructure rather than concentrated facilities

Europe’s painful energy security lesson of 2021-22 is being taught once again. Back then it was Russian pipeline gas, now it is Qatari LNG. If Hormuz remains effectively closed for any material length of time, Europe is once again in big trouble. That very much includes the UK, which remains highly dependent on gas imports. The spike may only be very temporary, but it would be surprising to see no Hormuz risk premium remain post-conflict. Higher gas prices flow through into higher power prices, especially in markets that has a high share of gas-fired power generation. This will further reinforce and accelerate the drive for reducing energy import vulnerability via electrification and buildout of local renewable generation and storage infrastructure.

In fairness, since 2021 European countries have been investing to reduce dependency on oil and gas imports. However, the job is nowhere near done - there is still a very long way to go. EU and UK gas imports have swung towards much greater reliance on US LNG as well as pipeline supplies from Norway. EU countries still import LNG from Russia, 4 years after the invasion of Ukraine.

Before this latest war, European leaders already showed a rapidly sharpening urgency about the need for faster transition as a key energy security strategy. They understand this US administration will follow its own perceived best interests, regardless of its European friends. The conflict further underlines that urgency.

As we write, the conflict is affecting sentiment and hitting the valutions of many European clean energy manufacturers, developers and utilities. However, the implications of this war are in fact very bullish for their longer-term prospects: they will be the backbone of future energy security in Europe. Share price weakness may in some cases create some opportunities to build long-term strategic holdings.

What next for Iran?

Iran is one of the world’s oldest and proudest civilisations, but this regime has long been on the ropes - with rampant inflation and an economy hollowed out among other things by years of sanctions. Its priority throughout has always simply been survival, amid fast-eroding domestic legitimacy. The brutal end to the recent uprising showed what lengths it will go to survive.

Now it is being decapitated from the sky, there are two most plausable succession scenarios. The first is that the Islamic Republic stumbles on in some curtailed, humiliated form, similar to how Hizbullah has operated after the assassination of Hassan Nasrallah and other top figures. The other is that a senior military figure or group steps into the power vacuum - perhaps an elite group of Revolutionary Guards. That would also be more continuity than rupture - as the regime has long been a religious overlay on a repressive military-commercial complex. Either way, Khamenei’s successors will be severely weakened and forced to comply with US and Israeli power, perhaps not dissimilar to the role Delcy Rodriguez has been obliged to play in Venezuela.

This may well happen within the next week or two. The big caveat is how long it really takes for Iran’s full military capabilities to be neutralised - hence they are going at it very hard. Before long the logic of diminishing returns will set in and Trump will have had enough.

Entirely different outcomes or timelines are of course possible. But what is also clear is that there isn’t an alternative faction closing in on power in the same way as there was in Syria in late 2024. We may yet be proven wrong, but it is hard at least at this stage to see how disparate groups of protestors or a popular youth-led uprising could meaningfully organise and assume power. It is equally hard to see how a US-backed figure like Reza Pahlavi could return and take over - something Trump is himself publicly expressing doubts about - or for that matter how Iran could seamlessly evolve towards a Western-style liberal democracy (even though its president is elected in the current system). The other obvious big risk is that as a multi-ethnic state, a peripheral part or parts of the country fall into regional ethnic or separatist conflicts, which would have wider implications across the region - but this is another whole analysis.

TTF Gas Benchmark doubles in a couple of days. Source: Trading Economics

Energy market trajectories

So Trump will declare victory as soon as he can possibly justify it - perhaps sooner. Already around 50 senior figures have been eliminated - by now most likely several more - and Trump is declaring they are ahead of schedule. So the victory lap could well be within the next week and or at least very likely within the first half of March.

That will likely bring a big drop in oil and gas prices, similar to what happened after the 12-day US/Israel-Iran war in June 2025, although not to the levels seen just prior to the conflict. It could conceivably happen much sooner if the Americans can prove Hormuz is passable - and if that passage is insurable. But right now that appears to remain a big if.

While the war continues, markets will remain nervous and oil and gas prices elevated. As we write, more facilities are coming under attack, such as the oil terminal at Fujairah. There will no doubt be more such incidents across the Gulf exporting countries - spreading into the Mediterranean too. Any significant Iranian strike on a vessel or key Gulf energy infrastructure could clearly send prices shooting much higher still.

Gas markets have been more volatile and therefore likely fall further when hostilities formally end. At that point, or whenever Hormuz security is restored and Qatari LNG production resumes, then from its Day 4 peak above €62/MWh we would expect the European TTF gas benchmark to fall back eventually into the €35-40/MWh range (equivalent to 90-100 p/therm for the UK NBP), up from just below €30/MWh pre-war. Likewise, we expect Brent oil front month futures would fall back from $80-85/bbl now to the $70-75/bbl range, again slightly higher than the pre-war $60-70/bbl band.

Pre-war, global gas markets looked increasingly well supplied, signalling progressively lower gas and power prices. But this war shows how quickly such an expectation can be put at risk, if not completely turned on its head. Slightly higher post-war prices will impact European gas and power markets, affecting both industrial and residential consumers. Power producers, especially those with more merchant vs long-term contracted revenues, will stand to benefit. Greater price volatility may also benefit flexibility providers such as operators of large battery portfolios.