ENERGIZED: Investment Insights on Energy Transformation

Edition 20

ETFs for the Energy Transformation

10 March 2026

Please note: This newsletter is for general informational purposes only and should not be construed as financial, legal or tax advice nor as an invitation or inducement to engage in any specific investment activity, nor to address the specific personal requirements of any readers.

Key Takeaways:

Besides the human suffering, the latest Middle East war is another stark reminder of the unsustainable vulnerabilities of fossil import reliance

This will likely reinforce global policy shifts and long-term capital flows into energy transformation

This underpins Energized’s fundamental rationale: to align with the financial flows that foster more secure electrified economies around the world

A convenient, cost-effective and lower risk way to do that is via Exchange Traded Funds (ETFs), although most have already recovered very sharply in recent months, so are now fully priced

However, after strong recoveries over the past year, most clean energy ETFs already look very fully priced, with trailing P/E ratios now in the 25-30x range

Of ~20 relevant ETFs, our top 5 shortlist seeks diversified long-term exposure to key markets, technologies and minerals: across Asia, electrification, solar, batteries, lithium and copper

The shortlist includes 2809, TAN, KGRN, LITM and COPX - profiles and rationales below

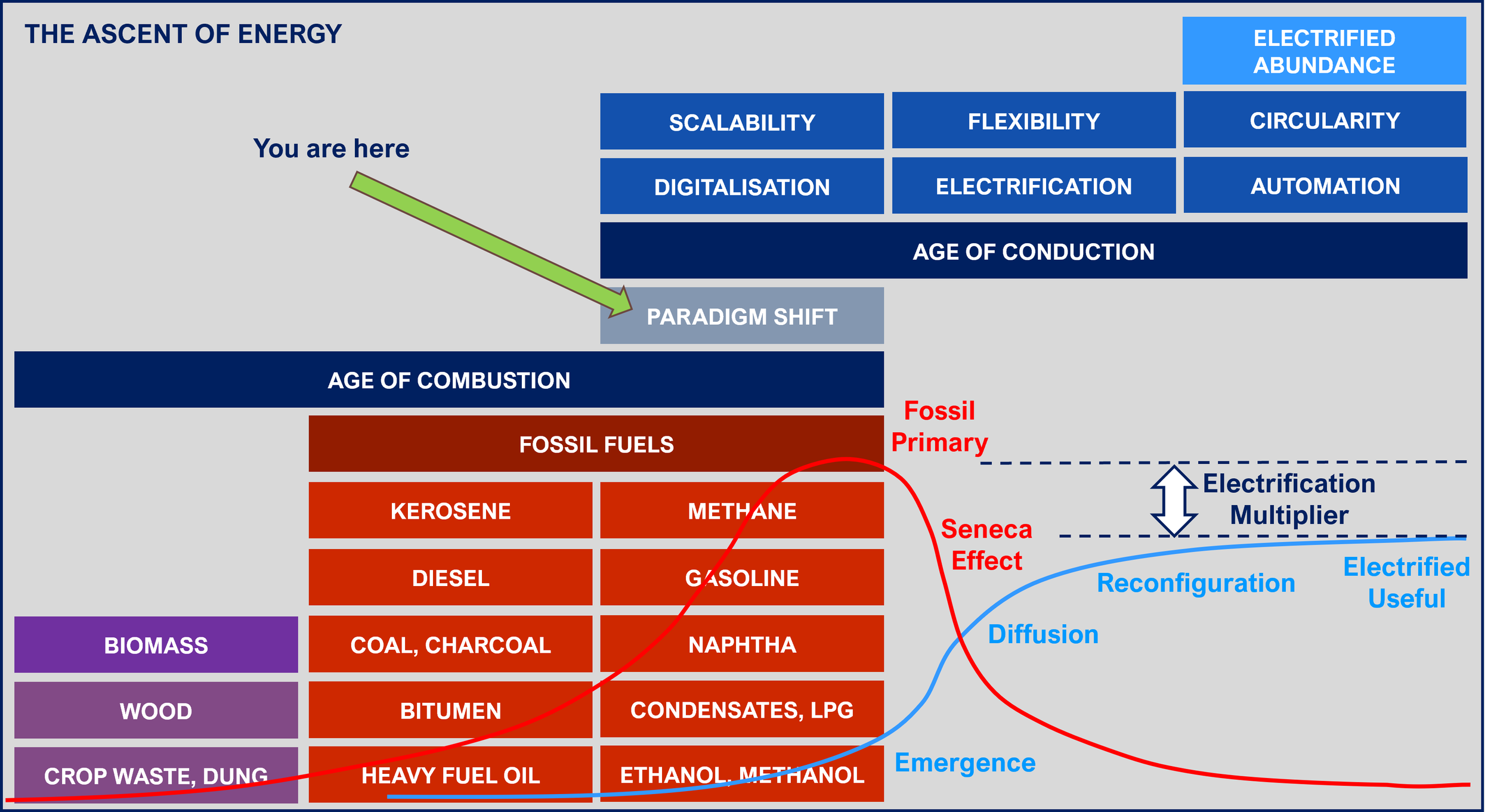

The Ascent of Energy

The key premise of this newsletter is that we have entered a pivotal period in global energy systems - the grey box in the schematic below. This is the apex of the Age of Combustion - in which all prior energy transitions mainly involved shifts in which type of carbon molecules were burned at faster rates than others. Equally, it involves rapid progress into the Age of Conduction, in which energy demand growth comes primarily - and eventually exclusively - in the form of electricity. This is in turn is bringing an investment supercycle in the hardware, infrastructure and technologies that underpin the key drivers of change: electrification, renewables, flexibility and efficiency.

The Ascent of Energy. Source: Strome - inspired by Max Roser’s “The Energy Ladder - What Energy Sources Do People on Different Incomes Rely On” (2021), which looked specifically at cooking and heating

Energy investing and ETFs

This pivot phase involves complexity and noise, as the prevailing system seeks to resist and obfuscate change. Through this noise, however, the signal is very clear. An inevitable civilisational transformation is underway, as countries, communities, companies and consumers all look for the most efficient ways to ensure secure and affordable energy supply and maintain habitable environments. The latest Middle East war can be seen among other things as just another episode in the painful final stages of growth in the legacy system. Ultimately it can only help to speed up the transformation.

The corollary is that, as investors, alignment with this civilisational process makes profound sense. Both in order to help build a better future and to generate positive long-term returns. In this phase, with careful execution, responsibilities and returns can be fundamentally aligned.

That is the rationale for Energized - not only as newsletter but also as portfolio, backing our own analysis to put our own money where our mouth is. The objective is to build up a balanced, resilient, long-term portfolio of 20-30 core strategic holdings that will stand the test of multiple business cycles, while aiming to diversify the sector concentration risks it as far as possible across geographies, technologies, currencies, business types and sizes. This portfolio is still in the fairly early stages of development - a future edition will cover the specific choices, performance and learnings from each investment in detail.

But in the meantime, many simply don’t have the time to commit to tracking individual stocks at the level required to keep properly up to date - let alone a full portfolio of them.

This is where Exchange Traded Funds (ETFs) come in. ETFs are an easy, relatively cheap way of getting broader exposure to a particular theme, sector or geography without getting bogged down in endless company-level analysis. Being effectively portfolios in themselves makes them less risky than more volatile individual stocks. They can also provide access to markets that are otherwise hard to invest in directly. So they’re certainly useful, albeit they’re not perfect either. For example, they can end up overweight on stocks that have already risen versus those still to do so (Bloom Energy is a notable example in this space). And what you gain in diversification you clearly give up in terms of control of what is included in the underlying basket of stocks.

Criteria

So how best to use ETFs to invest in the global energy transformation? Ideally we want diversified exposure across:

Geographies: Asia, South-East Asia, Europe, North America, etc

Themes: Electrification, Renewables, Flexibility, Efficiency

Company types: Manufacturers, developers, big integrated operators, smaller technology growth players, etc

Technologies / energy types: Solar, wind, grids, equipment, batteries, hydro, electrified transport - and their supply chains

We compiled and reviewed a longlist of around 20 relevant ETFs (identified in the list below by their stock tickers), considering which might offer the best potential for passive, diversified, long-term exposure to the global energy transformation. These are classified into several sub-categories below, which naturally overlap:

Diversified global clean energy equities: INRG, INRA or ICLN

Renewable power generation: RNRG or CNRG

Clean energy tech, electrification & batteries: CTEC or QCLN

China energy transition: KGRN, 2809 or 3134

Solar: TAN or 3134

Wind: FAN, WNDI or WNDG

Batteries & lithium: BATT, LIT or LITM

Copper: COPX, ICOP, COPP

Broader clean energy & environment: LIFE

Another important energy transformation investment theme is “grid” or “electrical equipment”. Although many of those companies turn up in other ETFs, there does not seem to be an ETF exactly designed for that.

Top 5 shortlist

In theory, we could spread across all of these, but a shorter list should give us sufficiently broad coverage, at least to get started. The selection then comes down to particular risk preferences, around jurisdictions, currencies and technologies. Based on ours, we have picked the top 5 that we plan to invest in:

Shortlist of 5 favoured energy transformation ETFs. Returns correct at time of writing. Source: Strome

Of course, others listed above may well prove better long-term choices, depending on risk preferences and objectives. But in combination, this shortlist should provide a healthy blend of exposure to the important energy themes and growth dynamics of the next decade:

Asian demand growth: much future energy growth (both supply and demand) will materialise across Asia, so getting direct exposure to that is essential. The Global X China Clean Energy ETF (2809) provides access to a variety of key names across the Asian electrification and renewables spectrum. Much future growth is already priced in, having already risen well over 50% in the past year, but it still remains down around 15% over the last 5 years.

Electrification: the growth of electrified transportation is another key theme, with a significant overlap with the Asia theme above. While the main focus is clearly electric cars, it also encompasses trucks, buses, trains and potentially eventually shipping (we are already seeing some early examples) - and even ultimately some forms of aviation, the final frontier of oil transportation demand. We include the KraneShares MSCI China Clean Technology Index ETF (KGRN) on the shortlist because it covers many of the key players in that space, such as BYD, Xpeng, CATL and Leapmotor. While we do have direct investments in both CATL and BYD in the Energized Portfolio, it is difficult to pick long-term winners in the highly competitive Asian electrified transport space, so the ETF is probably a safer route. KGRN is still only marginally up over the past year and down over 30% over the last 5 years.

Solar growth: solar has had its issues, but it can’t be ignored - it is the fastest growing form of energy supply and is going to have the biggest impact over the next decade (alongside batteries, which are a form of energy storage rather than production). So it makes sense to get some diversified exposure here to major manufacturers, developers, operators and solar technology players. Despite the difficulties experienced by major solar manufacturers in terms of market oversupply, the Invesco Solar ETF (TAN) has risen over 60% over the past year, but is still down over 40% over 5 years. Chinese policymakers have started to make efforts to address the structural oversupply issues in their solar industry, while there are signs that demand will eventually start to catch up as solar adoption scales globally outside of China. Our base case sees 655 GW of global solar installations in 2025 rising unevenly to 750 GW/pa by 2030, doubling total installed capacity globally to over 6 TW and tripling to over 9 TW by 2035.

Battery revolution: like solar, batteries / storage / flexibility is another huge growth theme that merits a place on the shortlist. Ideally we want something that includes manufacturers and the whole supply chain right down to the lithium companies. That is what the iShares Lithium&Battery Producers UCITS ETF (LITM) provides. That is already up around 70% over the past year and around 35% over the past 5 years.

Centrality of copper: along with lithium, copper is the mineral that will continue to play a critical role in enabling energy transformation, across the spectrum from high-voltage cables to key electrical equipment to EVs to battery storage. Many copper analysts are now forecasting a tightening market in coming years as new supply struggles to keep up with booming demand. The rationale for copper investment - as for lithium - is enough for another whole edition (to come). The Global X Copper Miners ETF (COPX) is the least volatile ETF to play this versus others that focus on smaller, riskier players. However, it is should be noted that this ETF has already more than doubled in the past year.

Rationales

Clearly, much more detailed analysis could be made on each of the chosen ETFs, but for current purposes a short overview is provided below.

1. Global X China Clean Energy ETF (HKG: 2809)

This aims to track the performance of companies in the Solactive China Clean Energy Index, which includes 36 industrial suppliers, technology companies, clean energy developers and utilities across the Chinese solar, wind, nuclear and hydro sectors. These are almost entirely Shanghai or Shenzen-listed companies that are hard to invest in directly.

After returning -19% and -31% in 2022 and 2023 respectively, it returned 3% in 2024 and 23% in 2025, and is already up again by a similar percentage in 2026 to date.

The fundamental rationale here is that these companies stand to benefit from China’s deep, long-term, strategic pivot towards an electrified economy. China is positioning itself as the world’s primary electrostate as a way to minimise dependence on imported hydrocarbons (it remains the largest absolute oil importer by some distance), harness the inherent economic efficiencies of clean energy technologies and to dominate the manufacturing of and trade in the next generation of energy infrastructure. Although the rollout of clean energy infrastructure will steadily internationalise, it remains highly dominated by China, which is expected to account for over 50% of new capacity installations over the next two years.

YTD return: 23.8%

1-year return: 63.7%

5-year return: 18.8%

P/E ratio: 26.6x

Total expense ratio: 0.68

2. KraneShares MSCI China Clean Technology Index ETF (NYSEARCA: KGRN)

This is another way to play the Chinese energy transformation, but with more focus on electrification and decarbonisation, as it features major EV and battery manufacturers.

It seeks to track the performance of the MSCI China IMI Environment 10/40 (USD Net) Index. This contains around 50 stocks across clean tech themes including electrification, renewable energy, sustainable water, clean buildings and energy efficiency.

EV manufacturers are a key constituent, with BYD, Li Auto, XPeng, NIO and Leapmotor all high up the list. Then there is battery hardware with CATL and BYD, clean utilities like China Yangtze and CGN Power, plus energy efficiency and digitalisation plays like GDS and Kingdee.

YTD return: 3.3%

1-year return: 5.6%

5-year return: -36.3%

P/E ratio: 19.1x

Total expense ratio: 0.79%

3. Invesco Solar ETF (TAN)

This is obviously another solar-focused ETF, this time based on the MAC Global Solar Energy Index, with 29 holdings across manufacturers, developers and technology leaders in this space. There is a broader geographical mix here of North American, European and Asian players in this case. The top ten holdings include: Nextpower, Enlight, First Solar, GCL Technology, Doral, HA Sustainable Infrastructure, Solaredge, Sunrun and Xinyi Solar.

Amid market uncertainty at the time of writing, it is down around 8% over the past month but has still had a stellar past 12 months, being up over 60% in that time.

YTD return: 10.1%

1-year return: 66.2%

5-year return: -44.4%

P/E ratio: 26.3x (28 Feb 2026)

Total expense ratio: 0.70%

4. iShares Lithium & Battery Producers UCITS ETF (LITM)

This ETF tracks the STOXX Global Lithium and Battery Producers Index, so is a way of playing the global battery flexibility revolution. It offers this through exposure through the value chain from lithium mining companies to compounds manufacturers and battery producers across a range of different geographies. It also “seeks to exclude companies classified as Non-Compliant by Sustainalytics’ Global Standards Screening (“GSS”)”.

The top ten holdings include: Albemarle, TDK, CATL, Furukawa Electric, PLS, Samsung, Panasonic, SQM, Mineral Resources and LG Energy Solution.

As lithium prices have started to rise significantly over recent months, this ETF has had very strong recent performance. That makes the near-term outlook likely to be volatile, but there is a strong case for a long-term exposure to lithium companies given the global growth trajectory as the dominant battery mineral over the next decade (more detail on this planned soon).

YTD return: 12.7%

1-year return: 70.1%

5-year return: 34.7% (since inception date 31/10/2023)

P/E ratio: 25.0x

Total expense ratio: 0.55%

5. Global X Coppers Miners ETF (COPX)

This seeks to track the Solactive Global Copper Miners Total Return Index, i.e. a basket of 40 copper mining equities. Unsurprisingly, the top ten holdings include many large copper miners and/or diversified miners that are heavily involved in copper extraction. It has also performed extremely strongly over the past year and is therefore certainly not cheap at this point, at least on a trailing price/earnings metric.

YTD return: 13.6%

1-year return: 118.8%

5-year return: 154.3%

P/E ratio: 29.6x

Total expense ratio: 0.65%

Is it now too late… or actually still early?

Many clean energy equities and ETFs underperformed over 2021-24, before reaching a low and recovering sharply over 2025-26 year to date. Some remain still well down over a 5-year period (admittedly an arbitrary cut-off point). As many leading energy transformation manufacturers, developers and operators have risen strongly in recent months, the ETFs on our shortlist now trade at trailing price/earnings multiples in the 25-30x range.

However, our investment timeline is not months or even years, but a decade or more, to capture the long-term upward trajectory of the global energy system shift. From that perspective, most of the growth may still to lie ahead, even if there are considerable fluctuations along the way.

At the time of writing we don’t know exactly how or when the latest Middle East war will end, so markets remain choppy and unpredictable. There’s no denying they have risen a lot over the past year and could easily experience a sharp fall if the conflict cannot be contained quickly. There is the risk of wider contagion and a financial shock or market crash, sparked off by the war or something else entirely. There is never a perfect time to invest.

What is clear, however, is that the extreme commodity price volatility caused by the closure of the Strait of Hormuz has once again exposed the energy security vulnerabilities of importing oil, gas, their derivative products and other essential commodities. Things may yet change, but it currently looks likely that the US may call a halt to this campaign without having successfully dislodged the Iranian regime, even if their military and economic resources have taken another severe hit.

Whatever the outcome, further short-term volatility may present opportunities for entry points into long-term portfolio targets, whether individual stocks or ETFs. But the deeper conclusion from an energy investment perspective is that we are likely to see more policies and money directed towards electrifying hydrocarbon importing economies and building out their renewables and battery capacities. This is the deeper signal emerging from the noise of war: such turbulence only strengthens the drive to electrify and insulate economies from such supply shocks.

Notes

PER = Price / Earnings Ratio (trailing year)

TER = Total Expense Ratio