ENERGIZED: Investment Insights on Energy Transformation

Edition 22

Batteries will change energy for good - and the revolution is still just getting started

23 June 2026

Towards a battery-based civilisation

The energy story of the last five years was the spectacular growth of solar power. From a negligible share pre-2020, it is on track to be the world’s largest single power source by the early 2030s. But that requires what will likely be the energy story of the next five years: batteries.

While the world’s attention is continually pulled back to the disruption to commodity flows through Hormuz, energy transformation investors have been focused on an equally significant development: the new frontiers being explored in energy storage and flexibility. It’s increasingly clear that battery technology will redraw the map for the future of energy, disrupting the legacy order across power grids, transport, data systems and industry. This is accelerating so fast that it’s almost a full-time job to keep up. This edition is a humble attempt to bridge that gap.

Our energy future is being fundamentally redesigned. Imagine the year is 2035. The energy infrastructure that underpins our civilisation looks very different than it did just ten years earlier.

How so? Fundamentally, energy still is the economy: without it, nothing works. Human civilisation remains predicated on the energy surplus, or return, between energy invested and harvested. That much remains unchanged.

But what has changed by then is the way we harness, store and consume that energy. Firstly, growth in final energy usage is exclusively in electric form. Next, growth in clean electricity supply not only outpaces growth in electricity demand, but total energy demand. Then, crucially, that incremental electricity gets cheaper, for two key reasons. First, because it is largely produced by abundant local, distributed generation infrastructure that harnesses effectively free resources. Second, because ubiquitous battery infrastructure enables that system to function by storing and releasing electricity wherever it’s needed: on the grid, in your workplace, in your home, across public infrastructure.

Our homes are more self-sufficient, less grid-reliant, digitalised energy systems, with automated software integrating efficient energy technologies including solar, electric heating and dynamic tariffs. But battery storage, either stationary or in our vehicles, will be the most critical element in making these systems work, enabling power to be stored and consumed when it has most value. By enabling the both grid-scale and residential energy services to be provided at lower cost, they will be the key reason why this energy system transformation will ultimately save money. The story of energy over the next decade is how we go from here to there.

Stationary storage is accelerating fast - but still only just getting started

There are actually two battery revolutions: stationary and mobile. We’ll cover the latter - aka electrified transport - next time. For now, suffice to say that we are still early in of one of the most consequential technology shifts in history: from internal combustion engine (ICE) vehicles to battery electric vehicles (BEVs). In 2020, the global market share of new energy vehicles (NEVs, i.e. battery electric (BEV) or plug-in hybrid-battery electric (PHEV) vehicles) was just over 5%. In 2025 it reached 25% and this year the International Energy Agency (IEA) expect it to hit 30%. By 2030, 50% global market share looks likely: ten countries across four continents have already passed this at a national level, most importantly including China, the world’s largest car market, which is now accelerating beyond 60% as the economic rationale for choosing NEVs over ICE vehicles gets ever stronger.

Here, though, we focus on the revolution in stationary storage, which is already the world’s fastest growing source of electricity dispatch. Most major economies, including the US, are racing to install new battery capacity, whether thanks to top-down official policies or permissionless bottom-up adoption, or a combination of both.

Please note: This newsletter is for general informational purposes only and should not be construed as financial, legal or tax advice nor as an invitation or inducement to engage in any specific investment activity, nor to address the specific personal requirements of any readers.

Disclosure: CATL is part of the Energized Portfolio

Key Takeaways:

There are two battery revolutions unfolding today: stationary and mobile - driving two energy transformation megatrends: flexibility and electrification

Stationary storage batteries are already the world’s fastest growing form of power dispatch and a real gamechanger for the next industrial cycle

Faster, cleaner and increasingly cheaper than new gas capacity, they are a Swiss Army knife for power grids, supporting the coming wave of 24/7 clean power and the “electrification of everything” from buildings and heating to data and industry

Consistent energy density and cost improvements are accelerating capacity growth: 2025 was ~50% up on 2024 and 10x higher than 2021

It’s still not too late to invest as the vast majority of additions are yet to come: we see global stationary storage capacity expanding 12x to reach 12.5 TWh by 2035

Mobile batteries are transforming transport, as range improves, costs fall and use cases expand from small EVs to large e-trucks

Both battery revolutions are key tailwinds enabling global battery leader CATL (HKG: 3750) to emerge as a Chinese industrial powerhouse

CATL’s dominance of the electrification and flexibility supply chains makes it a core Energized Portfolio holding, already up 40% to date since entry in January

Its strategy is evolving beyond one-off sales of its market-leading products towards a recurring service revenue model, targeting battery-swap networks in China and Europe

Although risks include mineral price volatility, OEM insourcing, commoditisation, tariffs and a China slowdown, recent share price trajectories imply that no matter which EV brands prove most popular, ultimately CATL still wins

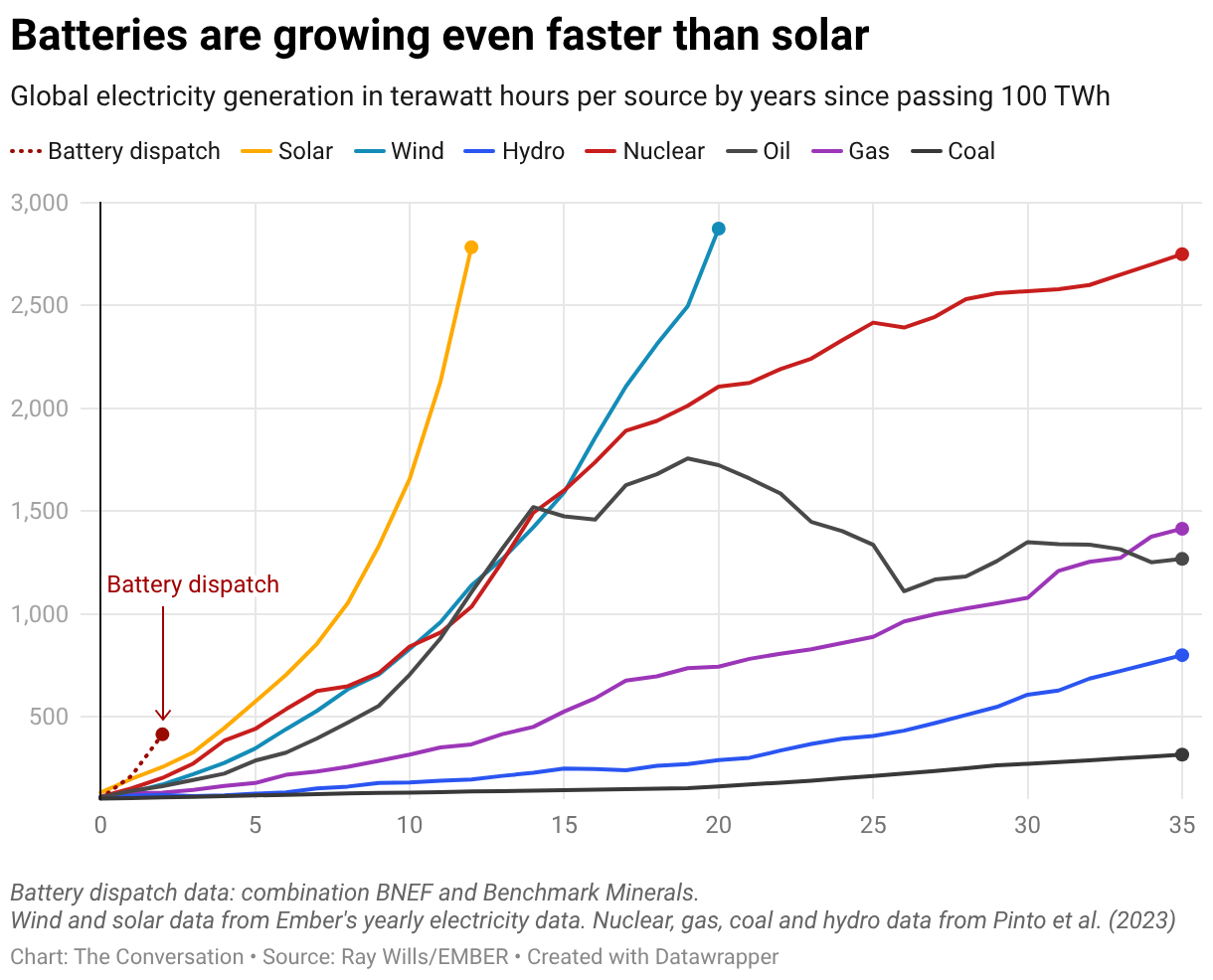

Pace of growth in battery dispatch vs other energy generation sources. Source: Prof Ray Wills / Ember / BNEF / Benchmark Mineral Intelligence / The Conversation

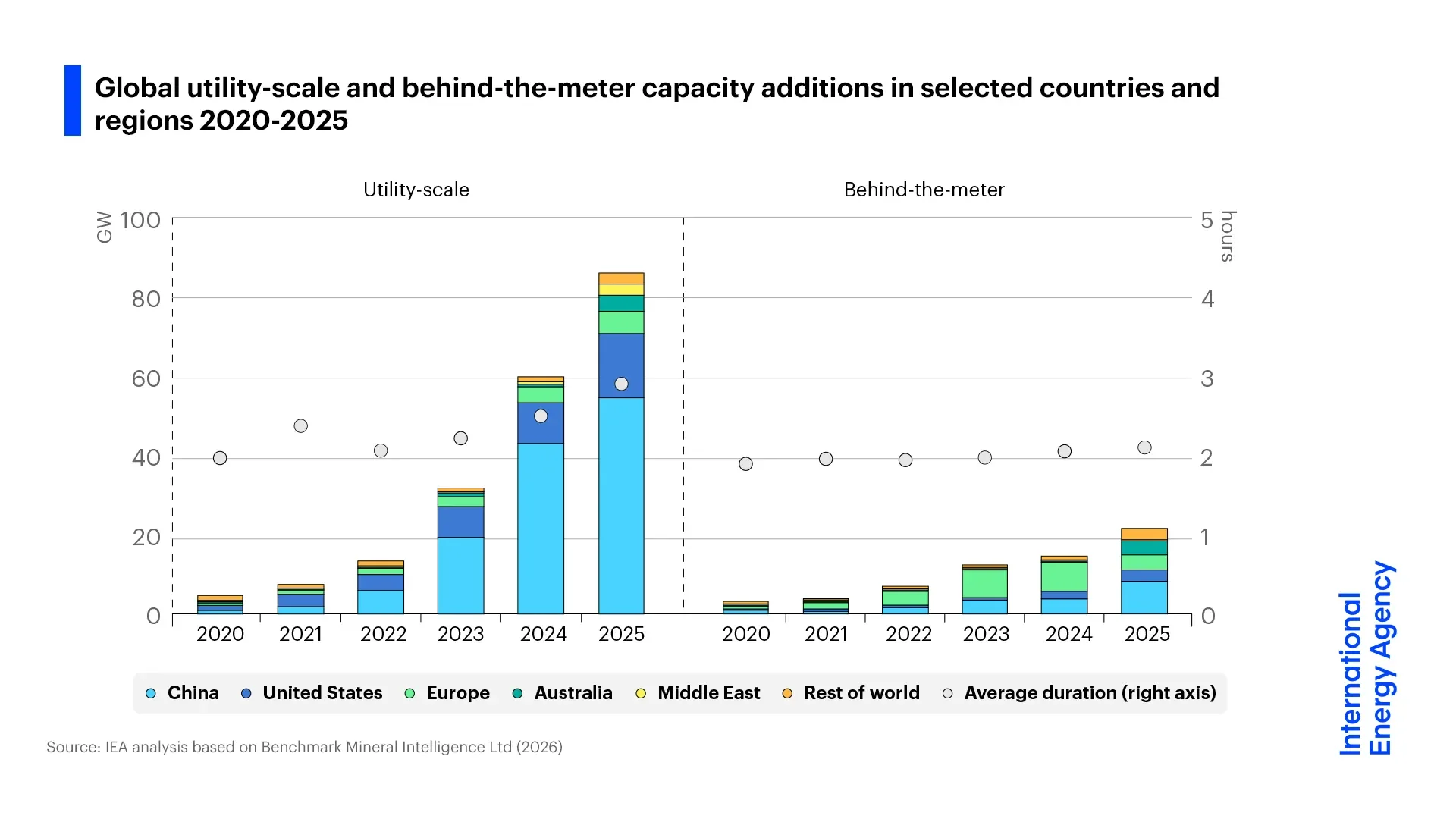

Stationary storage also falls into two categories: grid-scale (also known as battery energy storage systems, or BESS) and behind-the-meter (BTM), i.e. residential or commercial batteries that store locally generated power for the owner’s own use. The current global split is roughly 4:1. Both are dominated by lithium-ion batteries.

Global grid-scale and BTM battery capacity, 2020-25. Source: IEA

Batteries look set to go from marginal technology to pivotal role in a historically short timescale. BloombergNEF (BNEF) estimates 112 GW (IEA: 108 GW) of grid battery storage was installed in 2025. That is nearly 50% higher than 2024, and ten times the 2021 figure as adoption takes off. Over half of 2025 installations were in China, which grew by one third on 2024 and has by far the highest installed capacity. Elsewhere, the revolution is still just getting going, but lower absolute numbers means much higher growth rates. The US grew 60% by adding 19 GW, Australia surged from under 1 GW to nearly 8 GW, the Middle East (mainly Saudi Arabia) tripled to over 3 GW, UK almost doubled to 2.4 GW, and sub-Saharan Africa installations quintupled from under 1 GW to over 4GW.

Nearly half of Australia’s additions were behind-the-meter, i.e. homes and businesses directly insulating themselves from power price volatility. With batteries reaching 18% of dispatchable power capacity, Australia is fast evolving alongside California and Texas as a leading test cases for batteries displacing reliance on gas. This sets the template for other markets with high solar potential.

The average annual installation growth rate over the past five years is over 70%. BNEF projects the global annual installation rate to grow a further 41% in 2026 to 158 GW, passing 200 GW/pa by 2030. This implies a sharply decelerating growth rate in annual capacity additions as the installed base rises and the sector matures:

Actual and forecast battery energy storage additions, 2020-36F. Source: BloombergNEF

However, this looks likely to prove conservative, given the substantial unfulfilled potential across major markets. Energy transformation adoption curves are notoriously hard to predict, as the steep part in which a technology scales the fastest is by definition different to what comes before or after. The IEA has famously struggled with solar growth estimates. The battery curve is perhaps 5-10 years behind solar and will likely also surprise to the upside as lower costs leverage higher adoption. Our own model sees a steadier annual capacity addition growth rate, pushing new installations close to 500 GW/pa by 2035, versus BNEF’s ~300 GW/pa scenario.

It actually makes more sense to measure additions in GWh (the blue bars above), which represents total capacity factoring in duration, the number of hours for which each GW can perform at its full potential (see appendix below for definitions of battery terminology). The industry is trending towards longer duration, as longer-duration batteries typically have more commercial value, being better able to plug supply gaps. The higher the average duration, the more GWh of capacity is available for the same amount of GW. As it extends beyond 3 hours, we see annual additions exceeding 1,750 GWh globally by 2035. Cumulatively, that means around 12.5 TWh of stationary storage capacity would be installed globally by 2035.

The key takeaway here: by 2035 global battery capacity will likely be around 12 times higher than today, in GWh terms. And this could easily still turn out to be an underestimate.

Actual and forecast stationary energy storage additions, 2020-35F, in GW and GWh. Source: Strome FOREST model

Actual and forecast stationary energy storage additions, annual and cumulative in GWh, 2020-35F. Source: Strome FOREST model

If this sounds fanciful, it’s because we’re still in the very steep adoption phase. Many markets are more than doubling every year. The EU is targeting to nearly quadruple its storage capacity in just four years, from 55 GW in 2026 to 200 GW in 2030. The rationale is clear: electrifying the economy reduces dependence on imported oil (for transport) and gas (for power and heating). Whether or not such an ambitious target is met on time, this battery expansion will certainly change European energy markets.

A notable example is Spain, which continues to install renewables but has barely got off the starting blocks with battery storage. That is now changing rapidly, especially as battery costs fall and returns on battery investment rise. Projected capacity installation for 2026 (in GW terms) is over 15 times the level of just two years ago. More renewable generation capacity drives a clear need both for more flexibility capacity and grid resilience, as reflected in price volatility and last year’s blackout.

Grid-scale battery storage is finally taking off in Spain, among other European countries. Source: Ember

Such growth rates are pushing battery energy storage investment above $100 billion for the first time this year, with India, Latin America and the Middle East emerging fast alongside China, the US and Europe. The continued global growth in solar installations (665 GW in 2025, closer to 600 GW expected in 2026) maintains pressure on batteries to keep up and maximise the benefits of that new solar. The solar-battery installation ratio has fallen from 56:1 in 2015 to 6:1 in 2025 and is expected to reach 4:1 in 2026.

What’s driving such rapid growth?

The stationary storage revolution is happening for several inter-related reasons:

1. Flexibility

The International Energy Agency (IEA) calls batteries as the “multi-tool that can provide a range of system services at once”. They help to integrate every larger shares of renewable generation while also balancing and stabilising power grids. In other words, they provide system flexibility - a crucial feature of power systems which was hitherto mainly provided by dispatchable gas or coal plants. By soaking up excess power for later reuse, they solve the key challenge of renewable energy generation - its variability, or intermittency. That enables them to start to replace coal and gas in the continuous balancing of supply and demand, besides being faster response and cleaner to deploy. This is most visible in markets like California, where a rapid increase in solar and battery capacity from 1 GW in 2019 to 17 GW today means the grid now uses 61% less gas than only three years ago. The commercial value of flexibility is captured in the arbitrage between storing low or even negatively priced power for release when prices are higher.

2. Hybridisation

This flexibility also enables batteries to support the further growth of otherwise marginal or uneconomic renewable power. In systems thinking terms, that creates a mutually reinforcing positive feedback loop. Renewables and batteries each incentivise the other to expand, and that increased scale in turns also helps to improve efficiencies, reduce unit costs, and broaden use cases, which in turn enable further expansion. This is why much new renewable capacity is now hybridised, i.e. paired with either batteries and/or other types of generation, enabling renewable output to extend well into evenings and ultimately around the clock.

Recent analysis by the International Renewable Energy Agency (IRENA) showed that “in high-quality resource regions, firm renewable electricity has crossed the threshold of cost competitiveness with new fossil fuel generation”. The levelised cost of firm renewable power has fallen from >$100/MWh in 2020 to $54-82/MWh by 2025 in high-irradiance solar regions and strong wind corridors, versus $70–85/MWh for new coal in China and >$100/MWh for new gas globally. Major projects are already being built on that basis, like the UAE’s Al Dhafra solar-BESS complex which is reportedly delivering 1 GW of firm clean power at ~$70/MWh. This figure is expected to hit sub-$50/MWh in many regions by 2035, if not sooner, further increasing the relative attractiveness versus new thermal capacity.

Battery energy storage investment to top $100bn for first time in 2026. Source: IEA

Levelised cost of electricity for selected sites, combining solar and batteries, for 2025 and forecast for 2030. Source: IRENA

3. Economies of scale

The unit costs of solar PV and batteries have declined by 87% and 93% respectively between 2010 and 2024, thanks to manufacturing scale, supply chain efficiencies, design innovations and chemistry improvements. These decline curves are flattening, but still going. That means battery-firmed solar is becoming the fastest and cheapest means of adding new electricity capacity in many markets, even before the latest in an interminable series of Middle East wars pushed international gas prices up once again.

In some markets we are starting to see ever more affordable 4-hour duration lithium-ion battery systems used as at half-capacity, making them effectively 8-hour systems, to bridge the solar gap between sunset and sunrise. The path to around the clock clean power may turn out to be to simply overbuild such 4-hour systems to be able to discharge through the night, rather than wait for any of the various long-duration energy storage technologies to become more cost competitive.

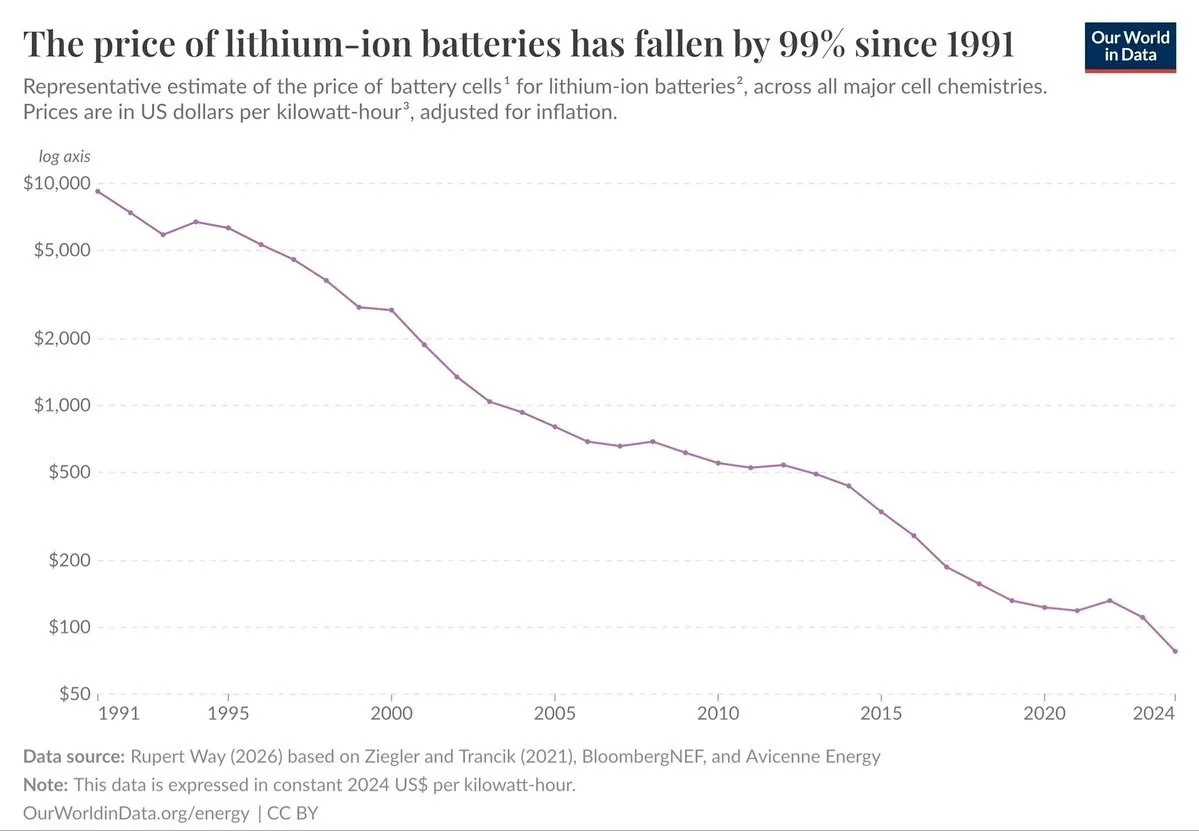

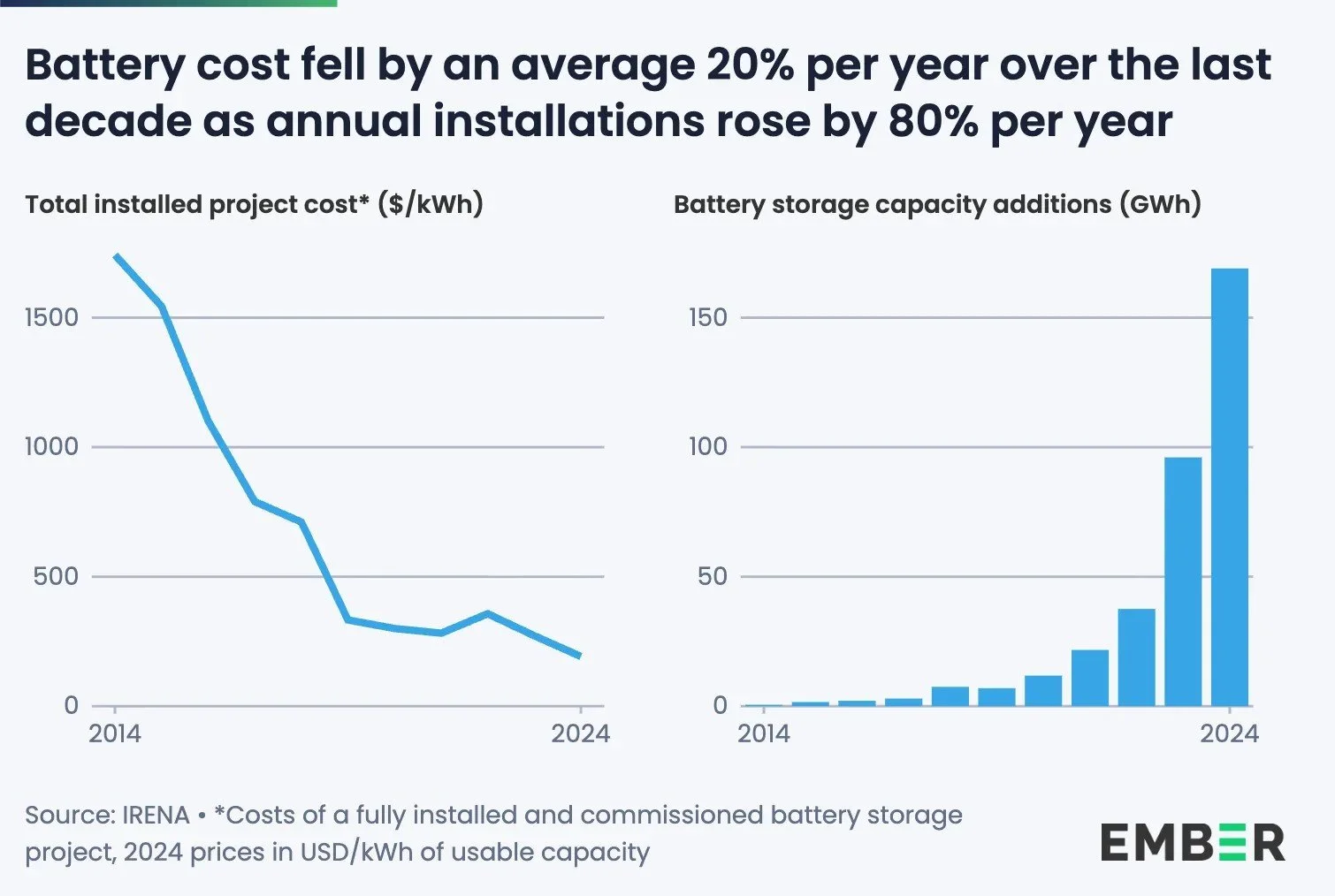

Ultimately, energy systems naturally coalesce around the cheapest available solutions. Over the last decade, continued price declines have taken batteries clearly through an adoption tipping point:

The dramatic fall in lithium-ion batteries since 1991. Source: Our World in Data

4. Modular resilience

As energy consumption electrifies and renewable output accelerates, grids have become the weak link. Insufficient transmission and distribution infrastructure means curtailments, congestion and price volatility. We can’t build tomorrow’s energy system on yesterday’s grid. That’s why investment in grids and associated critical equipment has been sprinting to catch up. But the answer is much broader than simply “build more grids”. Octopus Energy boss Greg Jackson has warned of the risk of huge malinvestment akin to building lots of giant shopping centres just before the rise of Amazon. It’s not just about investing more, but investing smarter.

This is where the battery revolution comes in. By storing and shifting electricity to when it’s needed most, batteries absorb supply-demand mismatches and help the whole organism to function more efficiently. By directly addressing points of maximum stress, i.e. power consumption peaks, they reduce the need to build expensive and time-consuming transmission and distribution hardware, providing much-needed resilience. Distributed energy infrastructure is inherently more resilient as it reduces the distance between generation and consumption. Modular batteries can be positioned everywhere, and stacked as necessary, supporting power systems across all their key nodes, at both grid scale and behind-the-grid, enabling more localised generation and consumption.

This is a key part of the evolution from centralised, top-down legacy power systems to the more diffuse, multi-directional emerging grid model. It also makes batteries an increasingly essential element of the new data economy, with its rapidly expanding needs for firm, reliable, uninterrupted power supply, ideally provided directly on site at data centres.

Beyond peak shaving, battery-based grid resilience also means the rapid-respones provision of ancillary services such as voltage and frequency control, which are essential to smooth and safe grid operations.

5. Speed to market

Battery modularity provides another critical advantage over just adding more gas, coal or nuclear capacity. In the new data economy, speed to market for new capacity can be as important as cost. Hyperscalers need power fast. Average construction times for grid-scale battery projects is 275 days, according to the IEA, with total project development timelines typically as short as 2 years.

6. Electrification

Finally, by helping to firm up renewable power generation and bring down the levelised cost of clean power, batteries will also help to electrify the so-called “hard-to-abate” sectors. These include industries that require high-temperature heat as an input, but also logistics and freight. Modular storage capacity enables the scale-up of electrified solutions that can replace fossil fuel reliance, such as electric arc furnaces, high-temperature heat pumps and electric trucks.

In parallel with cost declines, key metrics like energy density are consistently improving. In just a few years, 20-foot storage containers have doubled in energy density from 3-4 MWh to 6-7 MWh. The net effect is a continually stronger investment case, offering a long-term payoff of predictable, steady output, underpinned by rising electricity demand, that also involves no ongoing commodity risk exposure once installed. From individual to institutional level, capital is inevitably drawn in, transforming an edge case into a stable, logical infrastructure asset class, increasingly underpinned by supportive policies.

As battery costs fall, adoption has taken off. Source: Ember

The battery king: CATL

Who is leading this battery revolution? Internationally, clearly China, where 80% of batteries are manufactured today. Commercially, major manufacturers (OEMs) include China’s BYD, Gotion, CALB and EVE, Korea’s LG Energy Solution and Samsung, and Panasonic of Japan, which dominated battery manufacturing for many years.

But the undisputed leader for the foreseeable future is Chinese energy storage behemoth Contemporary Amperex Technology Limited (CATL), the world’s biggest battery maker, which defines itself as: “a global leader in zero-carbon new energy technology, committed to providing first-class solutions and services for global new energy applications, building a zero-carbon energy ecosystem with a comprehensive incremental strategy, promoting energy transition and sustainable development.”

If you haven’t heard of CATL before, there was also a first time you heard of Google or Amazon, or used Microsoft Windows. If batteries prove as indispensable to energy transformation as the internet, e-commerce or computing have been to modern economies, CATL is set to be the primary beneficiary. In fact, it has a strong claim right now to be the most important company in the global energy transformation, as the leading global EV battery supplier for the past nine years and leading BESS supplier for the past five - supremely well placed to benefit from both battery revolutions. EV batteries have historically dominated its sales, with BESS still only 2% five years ago. But as stationary storage takes off, the balance is shifting fast: BESS is now 25% of sales and expected to hit 50% by 2030.

Just 15 years since it was founded, CATL has firmly established itself as a leader in the highly competitive electrification ecosystem spawned by China’s long-term energy security strategy, designed to address the profound vulnerability of its unsustainable oil and gas import trajectory. Necessity is the mother of invention, and the industrial drive and innovation this has unleashed now has major implications beyond China’s borders thanks to the rapid growth in exports of batteries, EVs (mobile batteries) and solar PV.

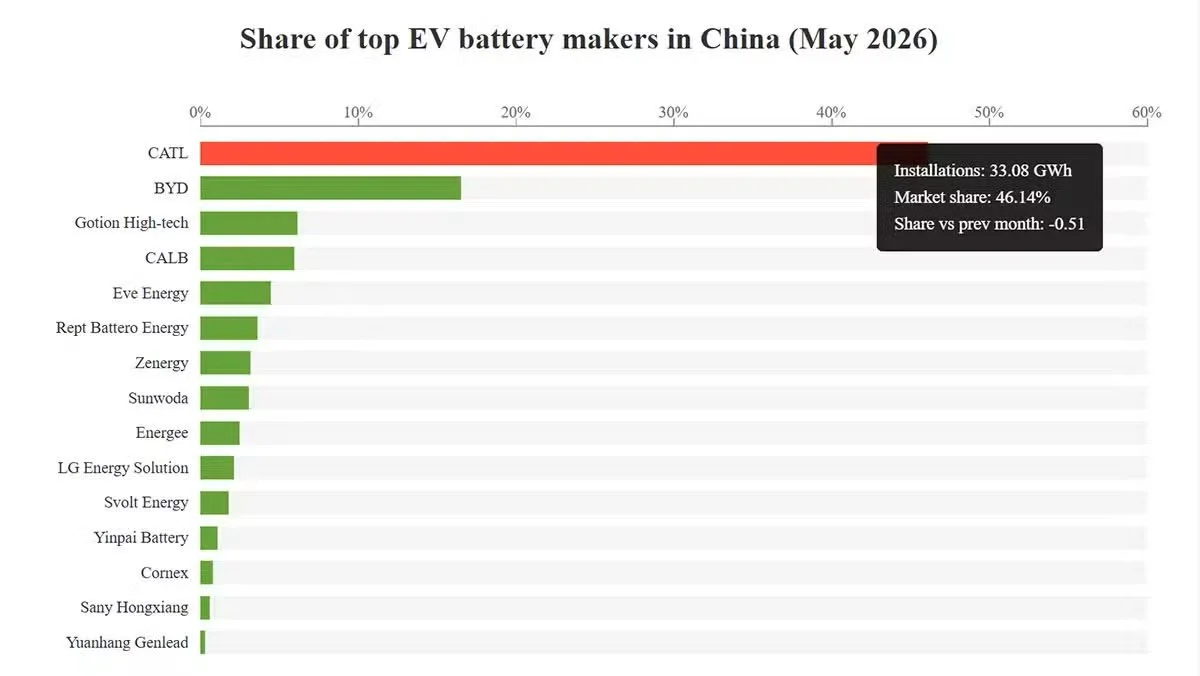

CATL’s share of domestic EV power battery supply stood at 46% in May, nearly three times the share of BYD’s 17%, while no others get beyond single digits. Its global market share in EV batteries is around 40% and in energy storage systems just over 30%. Maintaining such dominance will mean continuing to push the boundaries of performance and cost optimisation, but CATL appears best placed to do that - as well as potentially hoovering up smaller rivals as competition intensifies.

The rapid rise in the value of Chinese energy tech exports. Source: Bloomberg

CATL dominates Chinese (and global) EV battery manufacturing. Source: CABIA, CnEVPost

On the EV side, CATL supplies most major manufacturers, including Tesla, Geely, Changan, Chery, NIO, Li Auto, XPeng and Xiaomi, as well as major European brands that readers may be more familiar with, like BMW and Mercedes-Benz. For CATL, it barely matters which brand comes out on top in the great EV competition. Only BYD stands as a rival in manufacturing the batteries for its own cars. The trajectories in market valuations at least over recent months seems to support this thesis, with CATL strongly outperforming major automotive OEMs.

With the EU’s carbon tariffs coming into force, the next step is to shift from exporting batteries to exporting factories, serving fast-growing European EV markets from new manufacturing capacity within Europe itself. CATL’s new factory in Debrecen, Hungary, is set to open this year with Phase 1 production capacity of 72 GWh, alongside a planned 50 GWh joint venture in Zaragoza, Spain, with Stellantis.

Technology leadership

Technology leadership as well as manufacturing scale has been key to CATL’s market dominance. Its “Super Technology Day” in April 2026 showcased the latest product advances, setting new performance benchmarks across different applications. The highlights:

Third-generation Shenxing Superfast Charging Battery

10-15C superfast charging: 10%-80% charge in 3 min 44 seconds, with exceptional performance even down to −30°C

Superior lifespan: retains 90% capacity after 1000 cycles

Third-generation Qilin Battery: designed for premium long-range EVs

Energy density of 280 Wh/kg

Weight of 625 kg, 255 kg lower / 112 litres less than equivalent LFP systems

Enables 1000 km EV range, with 6% lower consumption per 100 km

10C superfast charging with 3MW peak power

Thermal-electrical separation improves safety

Qilin Condensed Battery: "the first application of aviation-grade solid-state technology in the passenger vehicle field"

High-nickel cathode and silicon-carbon anode

Energy density of 350 Wh/kg / 760 Wh/L

Weight <650 kg

Enables 1500 km range for sedans and >1000 km for large SUVs

Second-generation Freevoy Super Hybrid Battery

Extends all-electric range for hybrids to 600 km

15% higher range without increasing weight

10C superfast charging

230 Wh/kg energy density

Naxtra Sodium-ion Battery

Delivering GWh-scale sodium-ion industrialisation, with full-scale mass production by the end of 2026

Overcomes 4 key sodium-ion challenges: extreme water control, gas generation in hard carbon, aluminium foil adhesion, and self-forming anode systems

Fully integrated supercharging and battery-swapping solution

Designed to offer a unified system for home charging, public charging and battery swapping, rather than separate solutions, enabling “charge-swap synergy” at public stations

4000 charge-swap stations to be built across 190 cities and the national highway network in China by end of 2026 (there are currently 1470 existing ones across 99 cities)

Plan to co-invest with car manufacturers and energy partners to develop a “charge–swap sharing network” of 100,000 energy replenishment facilities by 2028, for seamless connectivity. Initial partners include Changan, Chery, GAC, Seres, SAIC-GM-Wuling, and BAIC.

The emerging strategy: an integrated supercharging-swapping network

This product range reflects a new industrial vision that targets continued, coordinated leadership across all chemistries and applications. Beyond competition for market share as mere supplier, the business model is now shifting towards being operator of a new energy infrastructure system - with batteries as the cornerstone. This aims to transition customer relationships from one-off battery sales to a recurring service model. By 2028, CATL plans to build 100,000 battery-swapping stations across China in alliance with major car brands. The idea is clearly to create a club that no car manufacturer can afford not to join, pushing CATL’s dominance further up the value chain. The latest batteries are designed as standardised, swappable units to fit seamlessly into this ecosystem so customers can easily trade up.

This week, CATL and Octopus Energy also announced that the battery swapping network is also heading for Europe. The “Swaptopus” joint venture will target the electrification of trucking, starting next year in the UK. The idea is to make trucking quicker, cheaper and cleaner, by charging up truck batteries when power is cheap to be ready to swap in for depleted batteries. This is already catching on quickly in China, reducing reliance on diesel. Electric truck battery swapping likely only works with industry wide standardisation, which is why CATL is best placed to enable it. We expect CATL and Octopus will likely also collaborate in future on commercialising Vehicle-to-Grid (V2G) potential in both geographies.

CATL EV battery swapping station in China. Source: CATL

The next frontiers of battery chemistry

Rapid battery innovation in Asia is redefining the potential of electric mobility all the way from small cars retailing below $10,000 to large e-trucks. The rollout of the Naxtra sodium-ion battery is now set to further raise the stakes. CATL is taking sodium-ion from theoretical concept as recently as 2020 to full commercialisation by 2027. This is the pace that other Asian and western manufacturers must compete with. Naxtra is already confirmed for Geely, Changan and Chery cars, and no doubt many others as cost and performance improves over time. But sodium-ion may have a bigger impact in stationary storage, where it can withstand extreme temperature ranges.

For batteries, the Wright’s Law learning curve has historically seen unit costs fall by around 25% for every doubling of production. Cost reduction can be about economising on a key input or eliminating the need for that input altogether. While overall battery costs derive from many different components, going beyond lithium to sodium effectively removes an entire line item. This promises to further accelerate the scale-up of stationary storage across grids and other use cases.

Then there is solid state battery technology, which could theoretically double current lithium-ion energy density to 500 Wh/kg. That would deliver increased capacity and driving range, even faster charging and, crucially, much safer performance and even better cycle life. CATL is clearly making progress here, but has expressed caution about the timeline for solid-state. Given its strong R&D division and track record to date, it would be hard to bet against solid-state commercialisation happening, even if its takes until the early 2030s. Meanwhile, the company’s electric aviation programme has reportedly been working on 4 tonne aircraft with 500 Wh/kg energy density. These research efforts are increasingly augmented by autonomous laboratories using large AI models to speed up product development, process optimisation and efficiency gains. This has reportedly already slashed the time required for screening new battery materials to optimise chemical formulas, especially in the drive for solid-state breakthroughs.

CATL’s chief scientist also recently confirmed its research into lithium-air technology, the ultimate battery holy grail. This is still very much in the moonshot realm, but if successfully realised it would dramatically reduce battery weight, complexity and reliance on minerals, enabling a theoretical energy density more or less on a par with gasoline. That would be orders of magnitude higher than current lithium-ion batteries or even next generation of sodium-ion and solid state batteries, opening up the final frontiers of electrification in applications like aviation. While this faces major technical challenges, it reflects an attitude of “nothing is impossible” ambition driven by deep commercial rationale.

Investing in CATL

CATL has been listed in Shenzhen (A-shares) since 2018 and added a Hong Kong listing in May 2025 (H-shares), making it more accessible to Western investors.

For the reasons above, if we had to choose one long-term investment for the battery revolution - or even the wider energy transformation picture - it would be hard to bet against CATL. That’s why it’s already the largest holding in the Energized Portfolio at 12% of the total. Since an initial investment at HKD 500 in January, it has already performed very strongly, rising by over 55% to a peak of HKD ~780 by early June, before falling back to just over HKD 700 at the time of writing.

As its core EV and BESS markets expand, CATL revenues and profits have grown fast. In 2025, revenues rose 17% year-on-year to RMB 423.7 billion, net income rose 42.3% to RMB 72 billion and earnings per share rose 39% to RMB 16.14. In the latest quarterly results, for Q1 2026, profits rose 48.5% year-on-year to RMB 20.7 billion, on revenues of RMB 129.1 billion, which were up 52.5% on Q1 2025.

While this is very impressive growth, the current H-share market capitalisation of HKD 2.13 trillion implies a trailing P/E ratio of 35x and forward P/E of 29x (at time of writing). There is clearly a lot of optimism already priced in, although Panasonic currently trades at an even steeper 53x earnings after a dramatic rise in valuation. Investing now implies a long-term view that both global battery revolutions are still relatively nascent and that CATL will maintain its leadership across both.

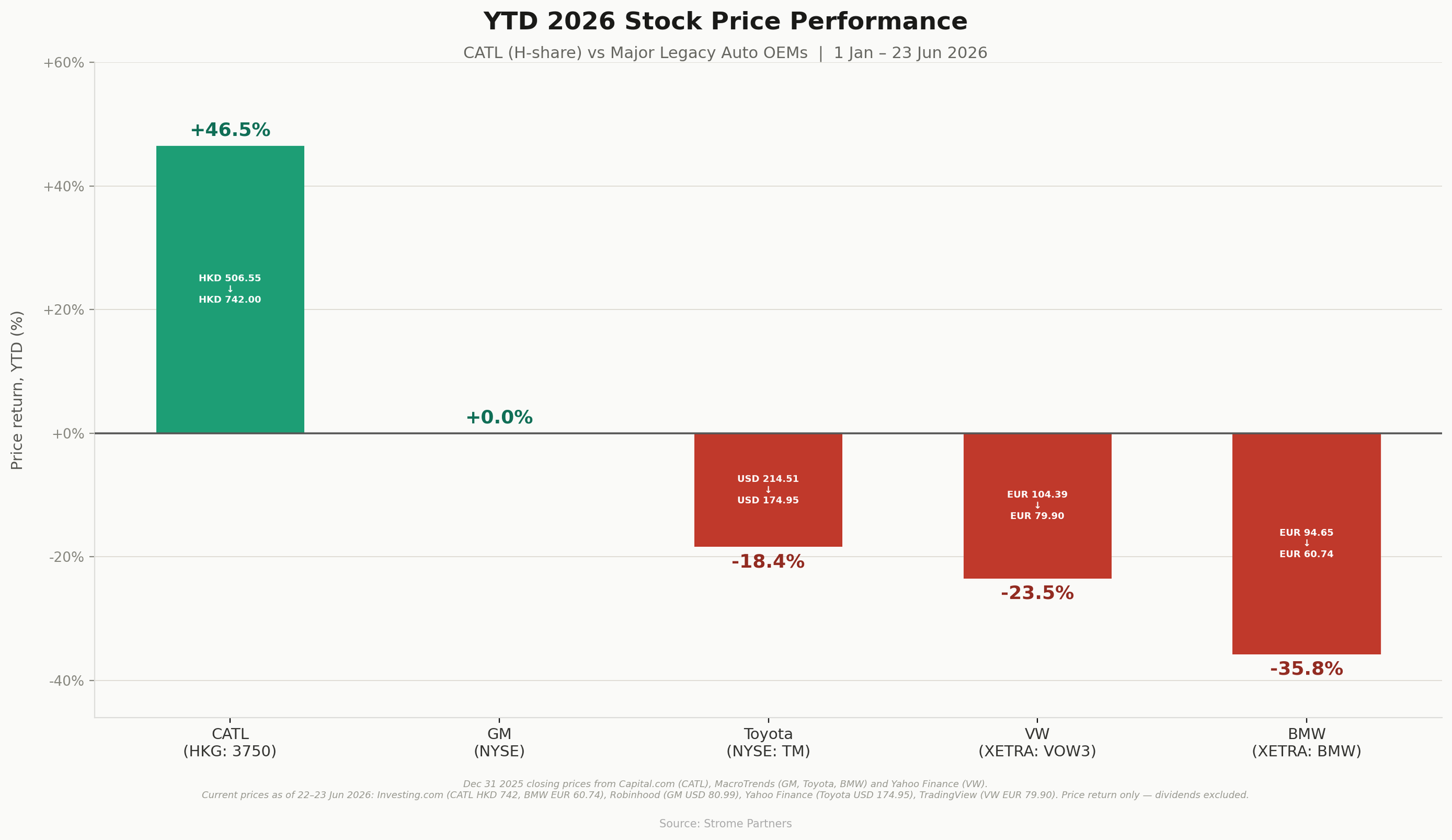

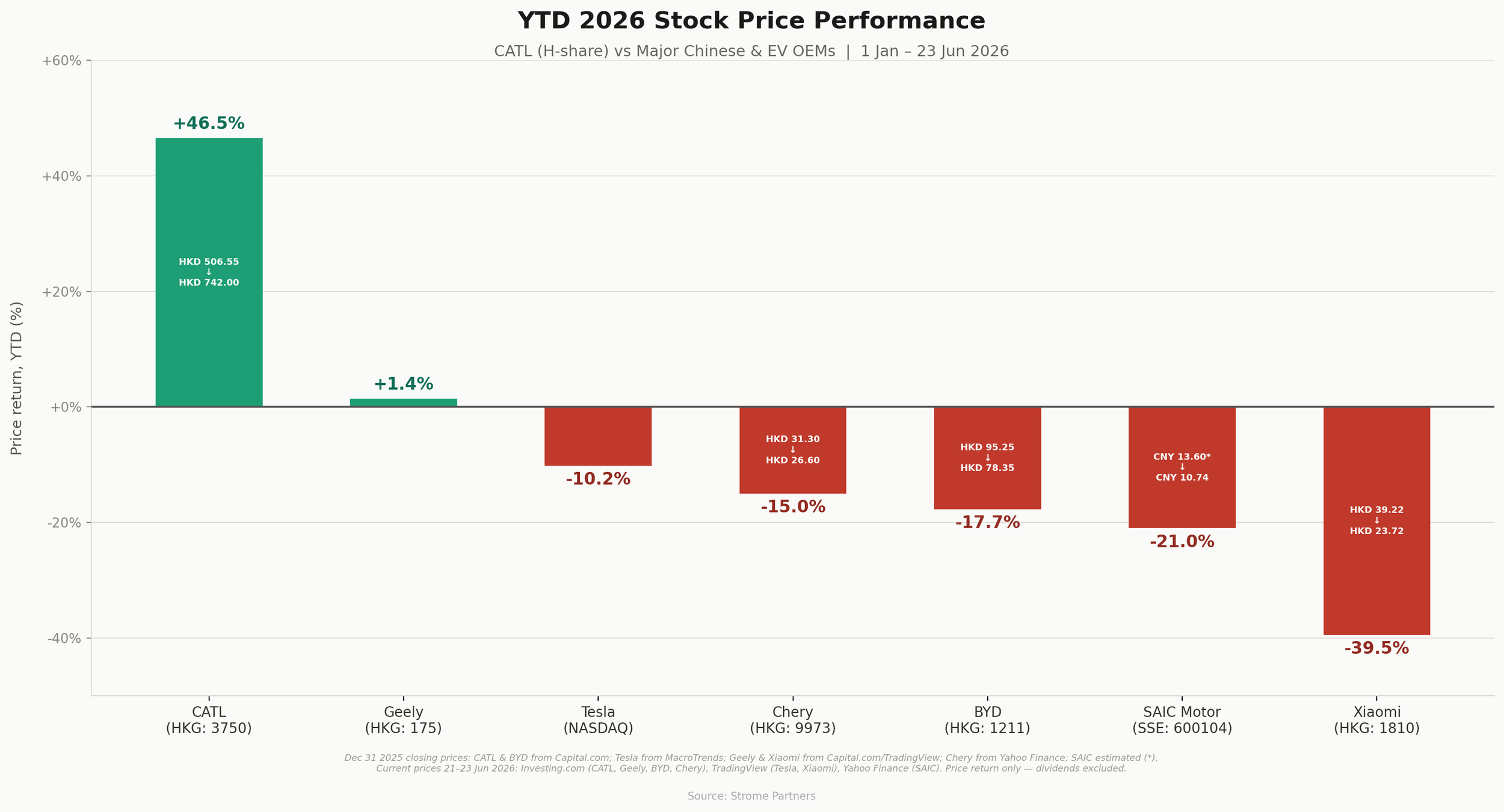

CATL’s dominant position among battery OEMs contrasts with the fierce competition for market share among its car manufacturer client base. The notable recent divergence in share prices between CATL and major ICE and/or EV manufacturers (many of whom are clients, like Tesla, Geely, SAIC and Chery) supports the thesis that the real value is being captured as battery supplier to such manufacturers (except BYD), rather than competing to sell cars to end consumers, especially as the Chinese new car market contracts.

CATL H-share YTD performance vs major car OEMs (GM, Toyota, VW, BMW), 22 June 2026

CATL H-share YTD performance vs major Chinese car and/or EV OEMs (BYD, Tesla, Geely, SAIC, Chery, Xiaomi), 22 June 2026

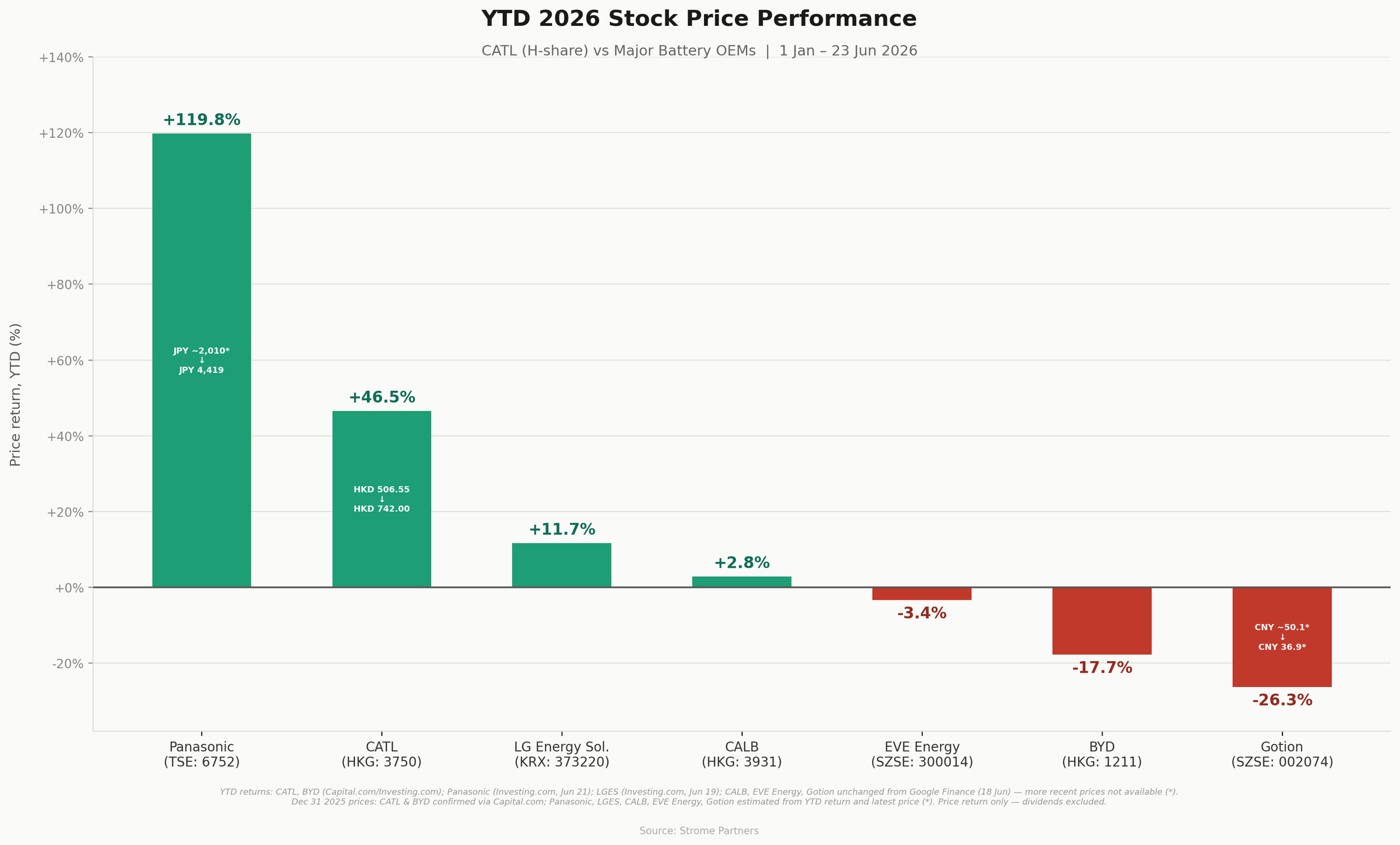

What about against other major battery manufacturers? CATL’s share have performed well versus competitors this year too, with the significant exception of Panasonic, which has more than doubled in value thanks to an aggressive pivot away from consumer electronics towards its stationary storage business. BYD’s weak share price looks more related to brutal Chinese car brand competition than its performance as a battery maker per se.

CATL H-share YTD performance vs major battery OEMs (Panasonic, LG Energy Solution, CALB, EVE, BYD, Gotion), 22 June 2026

Appendix: How to speak battery

There are several important criteria and metrics in assessing battery performance and commerciality:

Energy capacity: total battery size, measured in watt-hours i.e. kWh, MWh or GWh, depending on application. In vehicles, this translates directly into range.

Power: the rate of charge/discharge, measured in watts i.e. kW, MW, GW - the higher the number, the quicker it charges (if kWh is the size of a bath, kW is the speed that the tap can fill it up). Capacity additions are often quoted in MW or GW, but MWh and GWh give a more accurate picture.

Duration: length of time it can discharge its total energy capacity at its rated power. For example, a 100 kW / 100 kWh battery has a 1 hour duration, whereas a 100 kW / 200 kWh battery has a 2 hour duration (the same battery could also discharge at 50 kW for 4 hours, effectively extending duration at lower output). As longer duration grid-scale batteries can often capture more value, duration is generally lengthening across the industry, with 4-8 hour systems increasingly common. The average duration of new projects globally is now around 3 hours.

Gravimetric energy density: energy per unit of weight, measured in Wh/kg - how much energy can be packed in before it gets too heavy. Mainstream lithium batteries currently have an energy density of 250-270 Wh/kg.

Volumetric energy density: energy per unit of volume, typically measured in Wh/L - how much energy can fit into a certain space

Cost:per unit of energy, typically measured in $/kWh or $/MWh - how much energy capacity are you getting for your money

Safety: how flammable is the battery relative to others

Charging speed: time to charge up to a given capacity level, measured in minutes from one State of Charge (SOC) to another

Round trip efficiency: energy is saved or lost in each charge/discharge cycle

Lifespan: how long will the battery last before degrading, measured in total cycles

Temperature range: in which the battery can operate effectively, typically getting very wide for most applications

Self-discharge rate: the rate at which the battery loses charge if not used

Scalability: manufacturing capacity for a given battery and how easily can they be integrated into existing applications or systems

Some of these criteria are correlated while others have trade-offs. Which matter most depends on application: e.g. electric mobility vs stationary storage. EV drivers will typically prioritise maximum range and fastest charge for the cheapest cost, making energy density a key metric. BESS developers may be more focused on an optimal balance of cost, efficiency, duration and lifespan, as the asset must remain competitive over the long-term to get a return on their investment.

Investment risks

Insourcing: While Chinese car manufacturers are clearly taking market share away from legacy automakers outside of China, the brutal competition between them is also pushing them towards insourcing battery supply. CATL will need to remain technically and economically ahead to avoid ending up losing major customers.

Commoditisation: As a modular, manufactured product, batteries are inherently liable to commoditisation. Technical breakthroughs can be rapidly copied by competitors, limiting profit margins. The pressure will remain on CATL to continually preserve technical leadership and manufacturing economies of scale.

Mineral price volatility: prices of key inputs such as lithium, nickel, copper and aluminium can be volatile and are liable to keep rising as wider global energy transformation drives demand. CATL will likely aim to address this risk via a combination of engineering down or out the need for each mineral input and a embracing more vertically integrated business model, going upstream to source supplies directly and going downstream into recycling to limit the need for new raw materials.

Tariffs: trade risks are also a major factor, with both the US and Europe very keen to mitigate against the strategic vulnerability of excessive dependency on China while protecting local industries and jobs. CATL’s main strategy here is to go from exporting products to exporting factories: building new plants and or adapting brownfield sites in target markets. Its European manufacturing base is already being extended to Germany and Hungary, with Spain expected to follow.

China slowdown: As mentioned above, the Chinese car market has been slowing down, although this is affecting ICE vehicle sales relatively more than EVs. While this Chinese slump has an outsized near-term impact, other markets across Europe, Asia, Middle East and Latin America are much smaller but growing very fast. Ultimately we would expect global EV market growth to outweigh slower growth in China over the coming years.

Customer concentration: While CATL looks financially robust, it currently has accounts receivable of close to RMB 80 billion, but this looks reasonable at ~18% of sales and versus its formidable cash position of around RMB 350 billion (nearly USD 50 billion equivalent). Around 40% of its revenues come from five customers who face their own financial and strategic pressure. A major customer failure or car industry liquidity crisis could have a material knock-on impact, especially as it raises new debt to finance capex.

Cannibalisation: Finally, what if batteries get so good that consumers never need to replace them and the new car market effectively disappears? Right now such a scenario still looks very far off, given the gradual fleet turnover which lags the share of new sales metric by a long way. Even at the current 25-30% share of new sales, NEVs are still only around 5% of total cars on the road. As with stationary storage, the transport electrification revolution is substantially still to come.